|

||||

|

March

2019 |

||||

|

||||

| Forward | Subscribe |

||||

| Refer a Case | | | My Profile | | | Medicare Set-Asides | | | Download vCard |

Ensure That the Injured Party Is Still Standing After the Settlement Horn Sounds

Content for this newsletter courtesy of third-party administrator Ametros: download full white paper.

Content for this newsletter courtesy of third-party administrator Ametros: download full white paper.When an MSA account runs out of funds and reaches a zero-dollar account balance, Medicare agrees to step in as the secondary payer for ongoing and needed medical expenses as long as it is administered properly. Medicare highly recommends the use of professional administration to make sure these funds are extended as long as possible through discounts. If the funds are used and reported properly for medical care, Medicare will then step in as the payer.

The Pregame Analysis

Now let’s see how Joe, our fictitious injured party, best protects his future settlement dollars.

Let’s assume that Joe accepted a settlement with an MSA worth $200,000 and has a life expectancy of 10 years. He is expected to spend $20,000 a year on medical costs out of his MSA. While looking at these scenarios, it’s important to know that when the MSA has available funds, the injured party (Joe) pays 100 percent for all costs that are related to the injury and would be Medicare-covered. But how are costs paid for once the MSA is exhausted?

Upon verifying via reporting that the MSA was properly exhausted, Medicare will step up and cover roughly 80 percent of the costs, just like it does for any other Medicare beneficiary. That means Joe only needs to contribute about 20 percent to each treatment/procedure and Medicare will in essence “subsidize” the remaining 80 percent. Since Joe will have exhausted his MSA funds, he will need to rely on other personal funds to pay the Medicare copays/deductibles associated with his ongoing care.

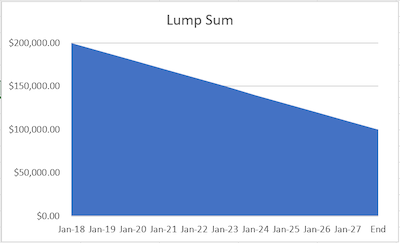

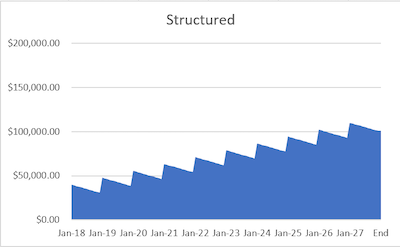

Case Scenario Playoff: Round 1

In this first, good scenario, let’s assume that Joe is doing well and is using professional administration to receive discounts so he only spends $10,000 a year on MSA medical items. Here’s a look at how the balances of his MSA account would look over the next 10 years with a lump sum settlement versus a structured annuity settlement.

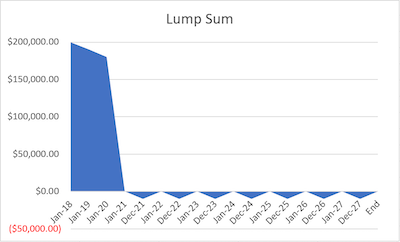

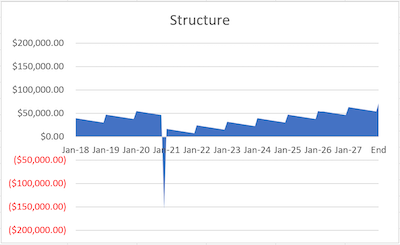

Case Scenario Playoff: Round 2

Now let’s assume that Joe is offered the exact same MSA settlement amount and starts out on the same pace, spending $10,000 a year. Unfortunately, three years after settlement, Joe needs to pay for a complex surgery that ends up costing him $200,000! Let’s see how the balances of his account change for the lump sum and structured scenarios.

The result is that while Joe spends more of his personal money in the year of the surgery ($30,700), when he has a structured annuity, he makes that loss up over time and actually ends up having about $71,400 in his account at the end of the 10-year period. This means Joe makes up the personal money he spent in the year of the surgery and ends the 10 years with a net gain of over $40,000 (which is the $71,400 he has remaining in his account less the $30,700 of personal funds he contributed). That is very significant considering the total settlement was only for $200,000!

In summary, the outcomes for Joe and his family can be strikingly different. With the lump sum settlement, he is losing $20,000 of personal funds and he never again has the chance to build value in his MSA account. With the structured settlement, Joe is actually better off over time, experiencing a net gain of over $40,000. The way Joe settled his case has a powerful impact on his finances. The difference between the two types of settlements amounts to over $60,000 to Joe, with a net gain of $40,600 from the structure compared to a net loss of $20,000 from the lump sum.

Trust Your Settlement Advisor as Your “Assistant Coach”

It’s important to keep in mind, not all professional administrators and annuities are the same. Choose an administrator that provides the best service and saves the injured party most on medical expenses. When choosing annuities, it’s important to work with your Ringler advisor to select a reliable, highly-rated life insurance company. Working together, we can help make sure the injured party is protected long after the settlement papers are signed.